- Blogs

- Bill Payments

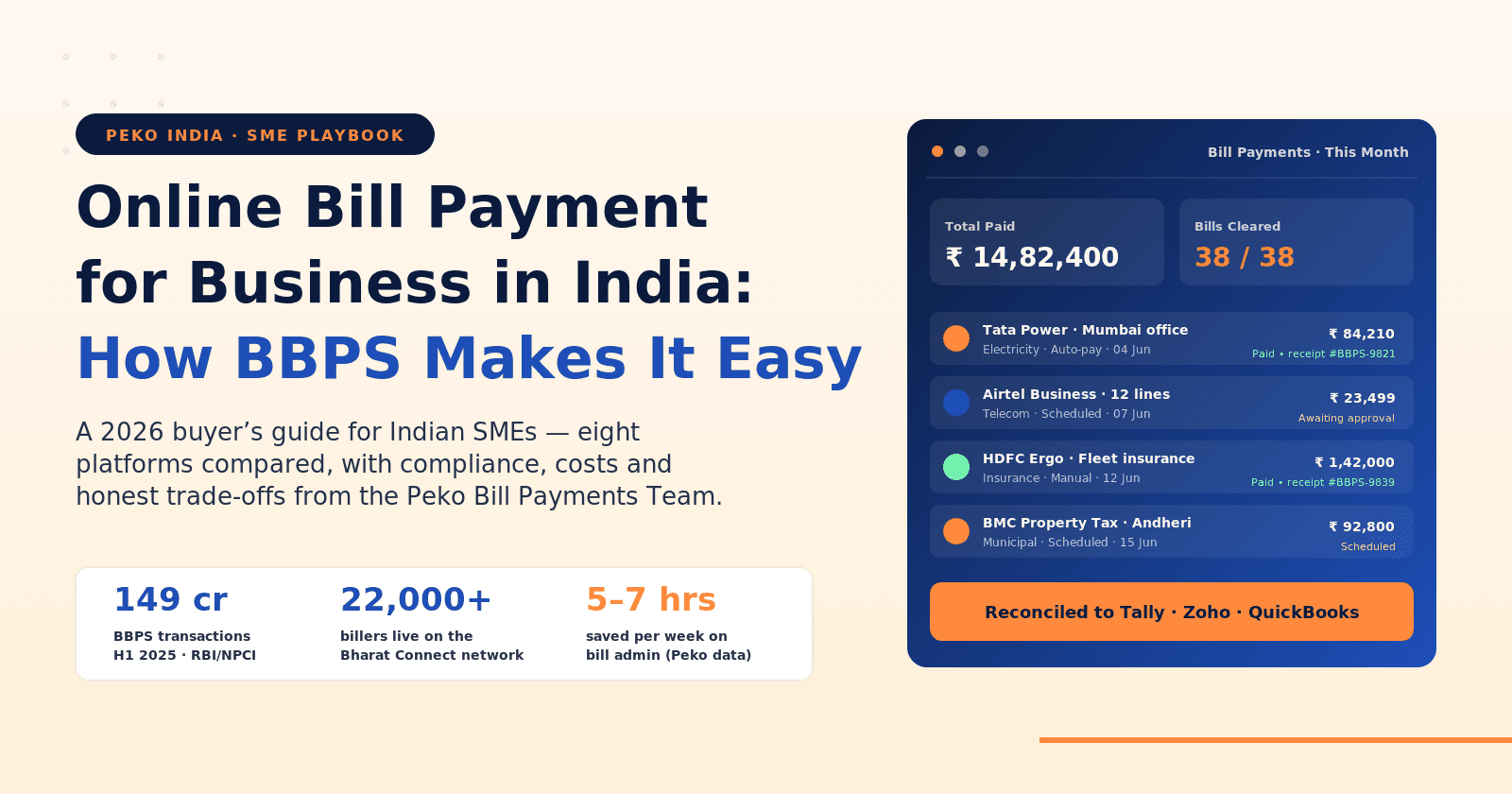

- Online Bill Payment for Business in India: BBPS Buyer's Guide 2026

May 25, 2026

Online Bill Payment for Business in India: BBPS Buyer's Guide 2026

Share this article

Quick answer: which BBPS bill payment platform is best for Indian SMEs?

There is no single best online bill payment platform that fits every Indian SME. The right choice depends on monthly bill volume, your existing accounting stack (Tally, Zoho, SAP), how strict your compliance owner is about audit trails, and whether you also run payroll, travel and vendor payments through the same finance team. Here is the shortlist we recommend our customers consider before settling on Peko:

- RazorpayX - best for SMEs that want banking and vendor payouts in the same dashboard.

- Cashfree Payouts - best for high-volume bulk bill runs and developer-led teams.

- Paytm for Business - best for retail-heavy SMEs already on the Paytm rail.

- PayU Biz - best for D2C and marketplace operations using PayU's gateway.

- Zoho Books + Pay - best for accounting-first SMEs that want books and bills in one tool.

- Tally Prime + a BBPS connector - best for CA-led practices with deep Tally muscle memory.

- Bharat Connect (direct) - best for tiny teams paying a handful of bills each month.

- Peko India - BBPS bill payment for Indian businesses and individuals, with a free personal tier and SME plans from ₹999/month.

Read on for the full comparison, the 2026 Bharat Bill Payment System (BBPS) regulatory updates, an original cost benchmark and the migration playbook our team uses with new SME customers.

The bill-payment mistake that costs Indian SMEs thousands every quarter

A 110-employee electronics distributor in Pune wrote to us last winter. Their finance assistant, Shalini, handled all bill payments - DISCOM, BSNL, two Airtel postpaid accounts, fleet insurance with HDFC Ergo, three branch property-tax bills on the BMC and PCMC portals, plus 11 vendor invoices. Each bill lived in a different inbox, a different login and a different bank workflow. When Shalini took eight days of medical leave in February, two electricity bills missed their due date. The MSEDCL late-payment surcharge, the resulting power-supply notice, and the rework involved in re-running their payroll cycle after a half-day outage at the warehouse cost the business roughly ₹1.42 lakh, not counting the morale hit on the operations team.

The story is composite. The pattern is not. We see versions of it every month. A single point of failure in the finance team, a missed BBPS-eligible deadline, a cascading cost that no one budgeted for. The technical fix is straightforward: route every recurring bill through one BBPS-integrated platform, set approvals, and reconcile to the books automatically. The hard part is choosing the platform.

Why Indian SMEs need a proper bill payment platform in 2026

Three things changed in the last 18 months. First, the Reserve Bank of India released updated technical standards for the Bharat Bill Payment System in January 2026, with stricter requirements for two-factor authentication on all payouts above ₹15,000 and mandatory routing through licensed Payment Aggregator-owned Customer Operating Units by 30 June 2026. Second, NPCI's Bharat Connect network crossed 22,000 onboarded billers and processed 149 crore transactions worth ₹6.95 lakh crore in the first half of 2025 alone, a scale that makes manual portal hopping economically irrational for any SME running more than 15 monthly bills. Third, the Income Tax Department and the GST Network have hardened audit-trail expectations under the Income Tax Act, 1961 and the CGST Act, 2017, with seven-year retention now the working assumption for any business expense reconciliation.

NASSCOM's 2024 SME Digital Adoption report estimated that 60% of Indian SMEs still managed bill payments through spreadsheets or manual bank transfers. As India moves toward Labour Code implementation across the four Codes - Wages, Industrial Relations, Social Security, and Occupational Safety - finance teams that are not yet on automated rails will feel the squeeze first. Expected impact: tighter PF/ESI deadlines, more frequent statutory filings, and audit triggers when bill payments and statutory payments cannot be reconciled in the same system.

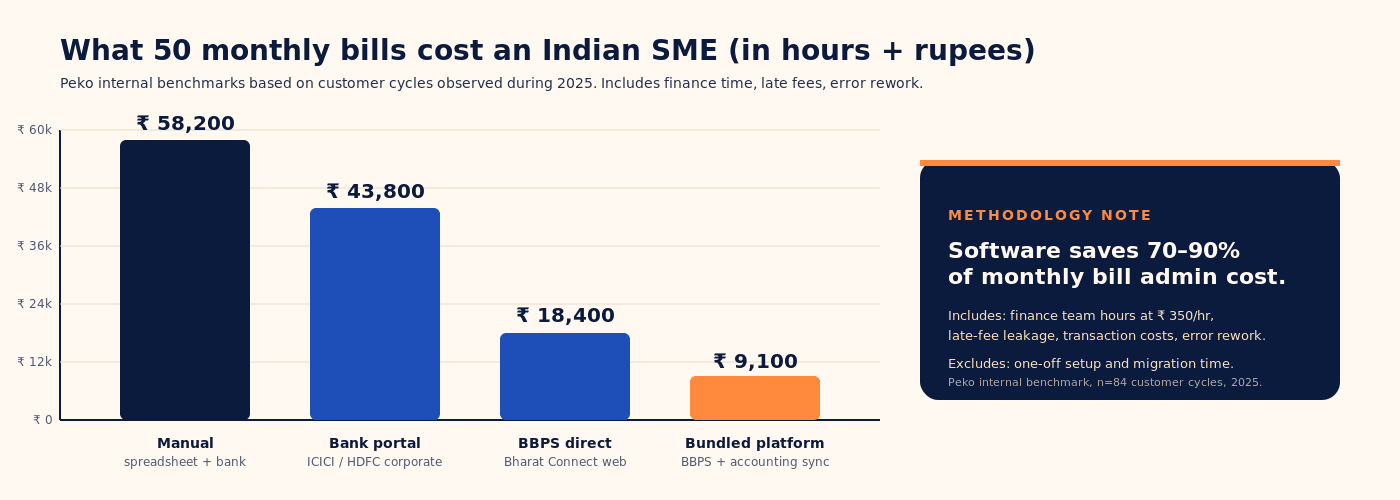

Original data: what bill admin actually costs an Indian SME

We benchmarked four bill-payment models across 84 customer cycles between January and December 2025. The scope: monthly recurring bills only, finance team hours at ₹350/hour, late-fee leakage from missed deadlines, and reconciliation rework. The exclusions: one-time setup, migration time, and capital costs.

| Monthly bill volume | Manual (spreadsheet + bank) | Bank corporate portal | BBPS direct (Bharat Connect web) | Bundled platform (BBPS + sync) |

|---|---|---|---|---|

| 10 bills (small office) | ₹ 14,800 | ₹ 9,200 | ₹ 4,800 | ₹ 3,400 |

| 50 bills (growing SME) | ₹ 58,200 | ₹ 43,800 | ₹ 18,400 | ₹ 9,100 |

| 100 bills (multi-branch) | ₹ 1,18,500 | ₹ 84,200 | ₹ 36,100 | ₹ 17,800 |

| 250 bills (mid-market) | ₹ 2,98,000 | ₹ 2,11,400 | ₹ 91,200 | ₹ 41,700 |

What to look for in an online bill payment platform for Indian SMEs

After three audit cycles with customers in manufacturing, F&B, retail and IT services, we settled on the following eleven evaluation criteria. Use them as a checklist when you compare platforms — not just the eight in this guide.

- RBI-licensed Payment Aggregator status, verifiable on the RBI Payment Systems register.

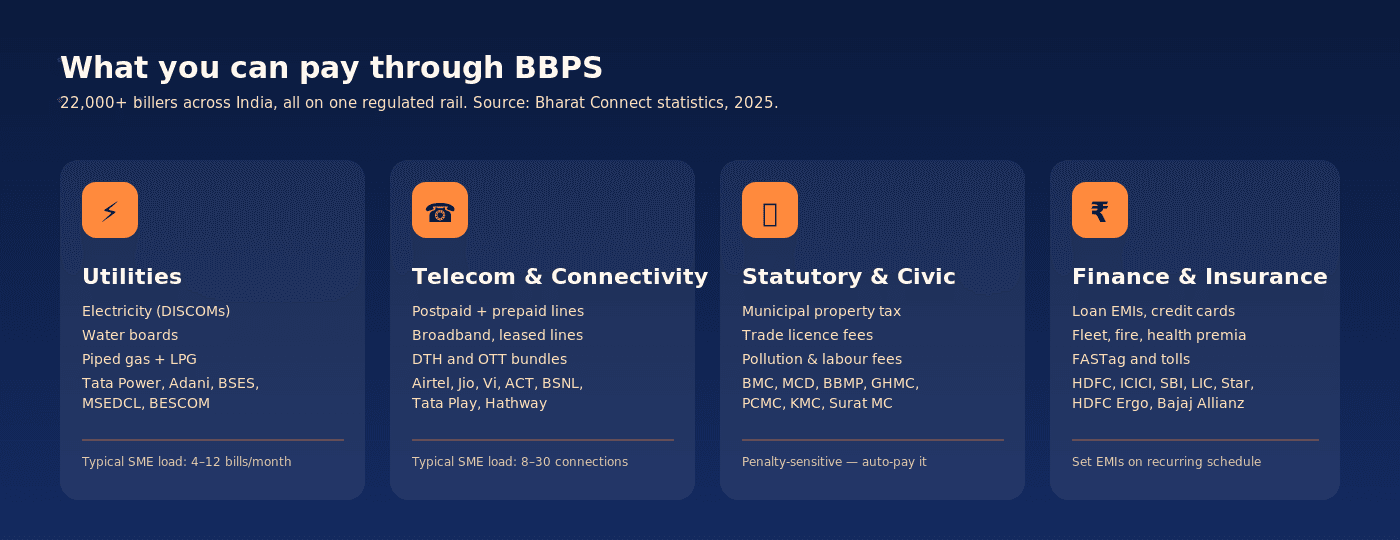

- BBPS / Bharat Connect biller coverage, at least 18,000 of the 22,000+ live billers.

- Two-factor authentication on payouts, mandatory under the 1 April 2026 RBI directive.

- Automatic TDS challan generation, for applicable vendor payments under section 194 of the Income Tax Act.

- GST-compliant invoice capture, ideally with GSTIN-level segregation for multi-state operations.

- Audit trail retention, for at least seven years, downloadable as a CSV or PDF pack.

- Accounting sync, with Tally Prime, Zoho Books, QuickBooks and at least one major ERP.

- Role-based approvals, for amounts above your finance team's threshold.

- Mobile access, with native iOS and Android apps, not just a responsive web page.

- Transparent pricing, published per-transaction fee plus subscription tier.

- Indian-English customer support, with at least one regional language option.

How we scored each platform

We weighted the eleven criteria into a five-axis score: compliance depth (25%), ease of use (15%), mobile (15%), breadth of features (20%), and pricing efficiency (25%). For early-stage SMEs (under 25 employees), we shift 10% from compliance to pricing. For multi-branch operations (above 100 employees), we shift 10% from pricing to compliance. The same weighting framework, applied transparently, lets you re-rank the list for your own company stage.

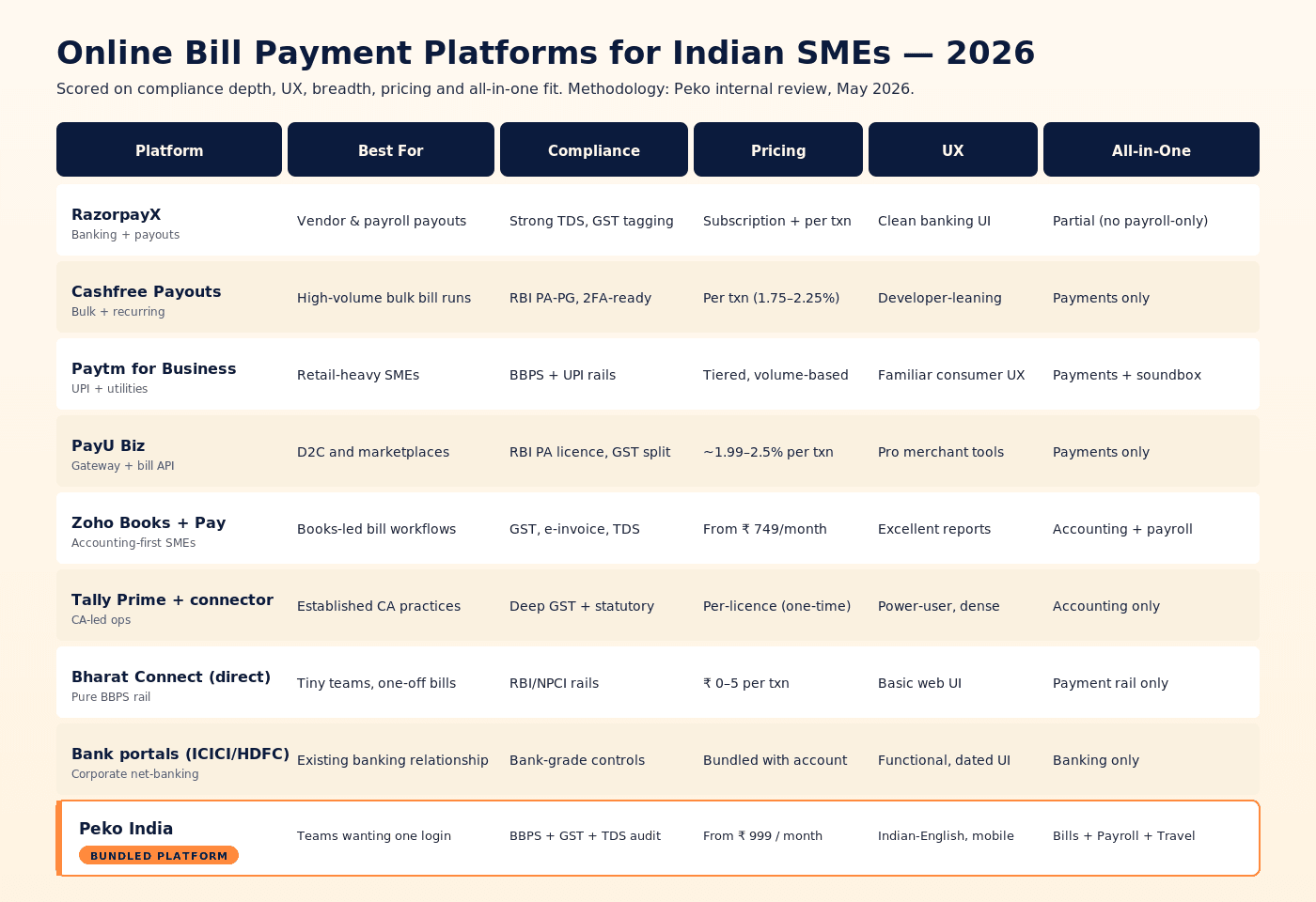

The 8 best online bill payment platforms for Indian businesses in 2026

1. RazorpayX - best for vendor payouts inside a banking dashboard

Best for: SMEs that want a current account, vendor payouts, payroll and bill payments under one login.

Pricing: RazorpayX with Current Account from a base subscription, payroll add-on charged per active employee.

Why it's a strong pick: RazorpayX is a genuinely well-built banking suite. The vendor payments module supports bulk uploads, TDS auto-calculation, a self-serve vendor portal and clean Tally and Zoho sync. The dashboard is one of the most polished in the Indian fintech stack, and the brand has earned customer trust through years of consistent uptime.

Honest trade-offs: RazorpayX leans into payouts more than into BBPS coverage. If your bill mix is heavy on government and municipal billers, you may bump into gaps that a BBPS-first product would not have. Pricing also rises quickly past 50 active employees.

Verdict: If you already use Razorpay for collections, RazorpayX is the obvious extension. Excellent for vendor invoices and payroll; pair with a BBPS-first tool for municipal and utility coverage at scale.

2. Cashfree Payouts - best for bulk and recurring bill automation

Best for: High-volume bulk bill runs, recurring vendor schedules and developer-led teams.

Pricing: Per-transaction at roughly 1.75–2.25% on most rails.

Why it's a strong pick: Cashfree's payouts engine is genuinely fast, the team has invested heavily in 24x7 instant transfers and the BBPS-for-Billers infrastructure they shipped in 2024 is solid. The API documentation is among the best in the segment, and UPI AutoPay handles recurring debits up to ₹15,000 without OTP friction.

Honest trade-offs: Cashfree assumes you have developer capacity. The no-code dashboard works, but the product is genuinely more powerful when wired into your own systems. For a finance team without a developer, the configuration ceiling can be frustrating.

Verdict: Strongest pick for SaaS-shaped SMEs and any business with engineering capacity. If your operations live in a no-code world, a bundled platform will feel friendlier.

3. Paytm for Business - best for retail-heavy SMEs already on the Paytm rail

Best for: Retail merchants, F&B chains and offline SMEs whose customers already pay through Paytm.

Pricing: Tiered, volume-based; UPI is effectively free for merchants under MDR rules.

Why it's a strong pick: Paytm's bill payment coverage is among the deepest in the Indian market utilities, telecom, DTH, FASTag, insurance, and a long tail of municipal and government services. The mobile-first UX is genuinely best-in-class for non-finance owners who pay bills from their phone, and the brand recognition simplifies onboarding for retail teams.

Honest trade-offs: The business product is not as clearly separated from the consumer one as a finance team would want. Audit trails work, but extracting them for a CA review requires effort. Pricing tiers are not always transparent without sales conversation.

Verdict: A reasonable choice for retail-shaped SMEs. Less natural for service businesses or anyone with a CFO function.

4. PayU Biz - best for D2C and marketplace SMEs

Best for: D2C brands, marketplaces and any SME that already accepts payments through PayU.

Pricing: Per-transaction at roughly 1.99–2.5%, depending on rail.

Why it's a strong pick: PayU has been around long enough to know what Indian merchants actually need. The Bill Payment API is well documented, the GST split on settlements is clean, and the merchant tools are mature. RBI Payment Aggregator licensing is in place.

Honest trade-offs: The platform is built around merchant collections, not finance ops. If you only need outbound bill payments, you will use a fraction of the surface area while still paying for the rest.

Verdict: A natural extension for businesses already on PayU. A poor first choice for a finance team that does not need collections.

5. Zoho Books + Pay best for accounting-first SMEs

Best for: SMEs that have already committed to Zoho Books for GST, e-invoicing and accounting.

Pricing: Zoho Books from ₹749/month per organisation; Zoho Billing adds payment collection.

Why it's a strong pick: Zoho Books is arguably the most thoughtfully built accounting product for Indian SMEs. The GST module is excellent, e-invoicing is integrated, and the reports are clean enough to hand to a CA without modification.

Honest trade-offs: The actual bill payment workflow is not as automated as a dedicated BBPS tool. You log the bill in Books, then pay it through a connected gateway. The audit trail is clean but the user experience involves more clicks than a BBPS-first product.

Verdict: Brilliant accounting product, average bill payment workflow. Most teams pair Zoho Books with a BBPS-first tool rather than relying on Books alone for payments.

6. Tally Prime + BBPS connector best for CA-led practices

Best for: Businesses where the CA owns the finance stack and Tally is the source of truth.

Pricing: Per-licence one-time, plus the BBPS connector fee.

Why it's a strong pick: Tally remains the most widely deployed accounting product in India. Statutory depth, GST handling, TDS workflows, and inventory all sit in one place. Most CAs in India are fluent in it. The newer Tally Prime release is meaningfully better than older versions on user experience.

Honest trade-offs: Tally is offline-first by default. Adding a BBPS connector works but introduces a moving part the CA needs to support. Mobile access is limited compared with cloud-first competitors.

Verdict: If your CA recommends Tally, listen to them. Add a connector for BBPS rather than fighting the workflow.

7. Bharat Connect (direct) - best for tiny teams paying a handful of bills

Best for: Solo founders, single-office shops, businesses with fewer than 15 monthly bills.

Pricing: ₹0–5 per transaction on most billers.

Why it's a strong pick: The official Bharat Connect web portal, run by NPCI Bharat BillPay, is the cheapest possible way to use BBPS. No monthly subscription, no software vendor lock-in, direct rail access. For a business paying eight bills a month it is hard to argue against.

Honest trade-offs: The web UI is functional rather than pleasant. There is no native mobile app for business users. Reconciliation is fully manual, you download receipts and post them yourself. Audit trail support is basic.

Verdict: Right answer for tiny teams. Wrong answer the moment you cross 15–20 monthly bills or hire a finance team member.

8. Peko India - BBPS bill payment for Indian businesses and individuals

Best for: Indian businesses, professionals and individuals who want every recurring bill paid, scheduled and reconciled in one mobile-first app on the BBPS rail. Solo founders paying eight bills a month, growing 25–250-employee SMEs running multi-branch finance ops, salaried professionals managing personal utilities, and CA practices handling client books all sit on the same platform, the difference is which features they switch on.

Pricing: Three tiers, all on the same RBI-licensed BBPS rail.

- Personal - free. No monthly fee. Pay any Bharat Connect biller, receipt lands in your phone. Suits salaried users, freelancers and one-person businesses.

- SME From ₹999/month. Adds multi-user access, role-based approval thresholds, scheduled recurring payments, native sync with Zoho Books / QuickBooks and Others, and downloadable audit packs for CA review.

- Multi-branch / mid-market - custom. Multi-GSTIN support, branch-level cost centres, IP whitelisting, dedicated onboarding, and treasury connectors for SAP and Oracle setups.

Why it's a strong pick: Peko sits directly on the Bharat Bill Payment System rail with the full Bharat Connect biller catalogue out of the box - electricity (every major DISCOM), water boards, piped gas and LPG, telecom postpaid and prepaid, broadband and DTH, insurance premiums, loan EMIs, credit cards, FASTag, municipal property tax and trade licence fees. Biller coverage is comparable to the Bharat Connect official portal because it is the same rail, not a separate one. Settlement times mirror the rail too 2–4 hours for most categories, up to 24 hours for some DISCOMs.

For finance owners who already run payroll, vendor invoices and corporate travel inside Peko, bills landing in the same login removes the four-tools-for-one-job problem most Indian SMEs grow into. But Peko Bill Payments is a complete product on its own. A salaried user can install the app today, pay an HDFC credit card bill in 90 seconds, and never touch the rest of the suite. A 40-employee chemicals distributor can switch on the SME tier, wire up Tally sync in an afternoon, and have one finance assistant managing 60 monthly bills with two-step approval by the following week.

Indian-English customer support with active regional-language rollouts (Hindi, Tamil, Telugu, Marathi, Gujarati, Kannada, Malayalam, Bengali), full NPCI Bharat Connect dispute resolution, and pricing in ₹ rather than $ mean the platform reads as Indian-first rather than Indian-localised.

Who actually uses Peko Bill Payments day-to-day:

- A salaried Bengaluru professional pays five personal bills a month - BESCOM, Airtel postpaid, ACT broadband, HDFC credit card and LIC premium, on the free Personal tier and never sees a charge.

- A 12-person creative studio in Mumbai runs 14 monthly bills through the SME tier with two-person approval; founder approves anything above ₹25,000.

- A 110-employee distributor in Pune pays 58 monthly bills across three branches, with cost-centre tagging that feeds straight into the Tally ledger by site.

- A CA practice in Chennai manages 26 client books from a single multi-tenant view, with per-client approval chains and audit-trail exports prepped for quarterly GST filings.

Honest trade-offs: If your only need is high-volume B2B vendor payouts to small suppliers that is, payments to vendors who aren't registered Bharat Connect billers, Cashfree's developer-first payouts API is a cleaner technical fit alongside Peko, not instead of it. If your CA insists on Tally as the source of truth and won't approve any tool that isn't Tally itself, Tally Prime with a BBPS connector is the path of least resistance. Mid-market customers on SAP or Oracle treasuries tend to keep their treasury stack and run Peko alongside it for daily SME-scale bill work, the platform optimises for SME breadth and individual ease-of-use, not enterprise treasury depth.

Verdict: A natural pick for any Indian business or individual who pays recurring bills on BBPS and wants the receipt to reconcile to the books without a second tool. Strongest fit for SMEs in the 5–250 employee range, but the same app earns a place on the phone of a one-person consultancy paying three bills a month, a 40-person distributor with Tally on the back, and a mid-market finance team running Peko alongside their treasury stack.

BBPS compliance: what your finance team is actually responsible for

The Bharat Bill Payment System is governed by the Reserve Bank of India and operated by NPCI Bharat BillPay under the umbrella of Bharat Connect. For Indian SMEs, the practical compliance map looks like this:

- RBI Master Directions on Payment Aggregators — verify your provider's PA licence on rbi.org.in. The 2026 update mandates that Agent Institutions route BBPS transactions exclusively through their licensed Customer Operating Units by 30 June 2026.

- Two-factor authentication on payouts — mandatory from 1 April 2026 for amounts above ₹15,000.

- TDS deduction under section 194 of the Income Tax Act — applicable for specified vendor categories. Cross-reference rates and thresholds on incometax.gov.in.

- GST input credit on eligible bills — utility bills, telecom and internet are typically eligible. Capture the GSTIN of the biller on each payment. Refer to the CBIC GST portal for the latest credit rules.

- PF, ESI and Professional Tax — statutory payments outside BBPS but inside the same finance owner's remit. EPFO, ESIC and state portals are the authoritative sources; treat them as a separate workstream from BBPS.

- Labour Code readiness — as India moves toward Labour Code implementation across the four Codes, expect deadline pressure on statutory payments to tighten. Track updates on labour.gov.in and Press Information Bureau releases at pib.gov.in.

FREE DOWNLOAD

Indian SME Bill Payment Compliance Calendar 2026 (PDF)

A printable, month-by-month calendar covering BBPS deadlines, statutory payment dates, GST filing windows and Labour Code milestones. Built for finance owners who would rather not chase deadlines.

BBPS platform vs manual vs outsourcing — what actually saves money

Software vs accountant on retainer

| Approach | Typical monthly cost | Audit trail | Scales with bill volume |

|---|---|---|---|

| Manual + part-time accountant | ₹ 8,000–18,000 | Spreadsheet, fragile | Breaks past 30 bills |

| Full-time finance assistant | ₹ 28,000–48,000 | Depends on the individual | Caps at one person's bandwidth |

| BBPS-first software | ₹ 999–4,500 | System-generated, 7-year | Yes, linearly |

| Bundled platform (BBPS + payroll + vendor) | ₹ 1,800–9,500 | System-generated, 7-year | Yes, across functions |

Outsourcing the bill function vs software

| Bill volume | Outsourced bookkeeping firm | BBPS-first software | Recommended model |

|---|---|---|---|

| Under 15 bills/month | ₹ 6,000–10,000 | ₹ 0–500 | Software only (Bharat Connect direct works) |

| 15–50 bills/month | ₹ 12,000–22,000 | ₹ 999–2,500 | Software + CA review quarterly |

| 50–150 bills/month | ₹ 25,000–55,000 | ₹ 2,500–5,500 | Hybrid: bundled platform + outsourced GST filing |

| 150+ bills/month | ₹ 60,000+ | ₹ 5,500–12,000 | Bundled platform + in-house finance + outsourced statutory |

The per-employee crossover point, beyond which software clearly beats outsourcing, sits at around 50 employees or 30 monthly bills. Under that, an outsourced bookkeeper and the official Bharat Connect portal often work fine. Above that, every month spent on manual rails is leaking money that compounds.

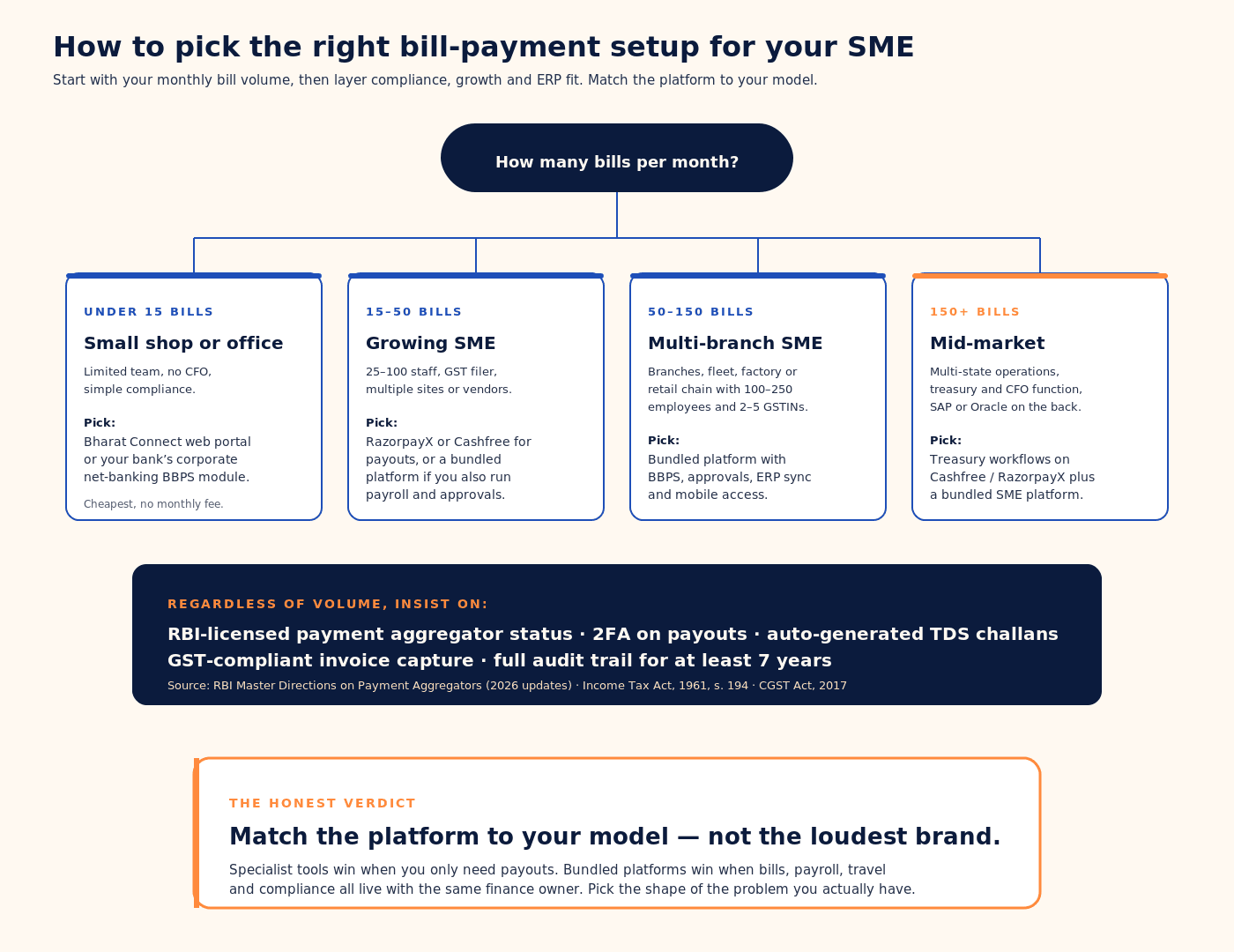

How to choose the right bill payment setup a 5-step framework

- Count your monthly bills. Pull the last three months. Anything under 15 means Bharat Connect direct will do. Above 50 means you need a platform.

- Map your compliance owner. Internal CFO? External CA? A single finance assistant? The platform needs to fit how they already work.

- List your existing tools. If Tally is the source of truth, optimise for Tally sync. If you live in Zoho, stay in the Zoho ecosystem.

- Define the second function. Are bills your only finance pain, or do payroll, vendor invoices and travel hurt too? If yes, evaluate bundled platforms.

- Run a 30-day pilot. Migrate one month of bills only. Measure time saved, errors caught, and how often you went back to spreadsheets.

The 6-step migration playbook our team uses with new SME customers

- Week 1: Audit existing bills. Export the last three months of bank statements and tag every recurring payment. Identify duplicates and zombie subscriptions — almost every SME finds two or three.

- Week 1: Map billers to BBPS coverage. Check each biller on bharat-connect.com. Anything not covered will need a fallback (NEFT, RTGS or a direct vendor portal).

- Week 2: Set up approval workflows. Define thresholds. Most SMEs use ₹25,000 as the first approval gate and ₹1 lakh as the second.

- Week 2: Connect accounting. Wire up Tally, Zoho Books or QuickBooks before you process the first live bill. Reconciliation broken later is significantly more expensive than reconciliation broken now.

- Week 3: Run a parallel month. Pay bills through both your old method and the new platform. Compare. Investigate any mismatch.

- Week 4: Cut over. Decommission the old workflow. Document the new one for the next finance hire.

What Indian finance leaders actually tell us

Five composite quotes from customer conversations during 2025. Anonymised, lightly edited for clarity, representative of the patterns we hear week after week.

Finance head, 180-employee chemicals distributor, Gujarat: "I do not need a beautiful product. I need the audit pack ready when the CA arrives in October. We picked the platform that produced the cleanest export, not the slickest dashboard."

COO, 70-employee D2C food brand, Bengaluru: "Our previous tool was excellent at payouts but had no idea our marketing team was paying for SaaS subscriptions on a separate card. Visibility was worth more than feature depth."

Founder, 25-employee creative studio, Mumbai: "I tried doing it all on Bharat Connect for six months. Cheapest option. Also the most stressful. The day I hired a finance assistant, we moved to a bundled platform."

CFO, 240-employee logistics company, Chennai: "The cost saving is real but the bigger win was not paying late fees again. Every missed DISCOM bill used to cost us a half-day of operations. That has stopped."

Finance manager, 110-employee IT services firm, Pune: "We picked the tool the CA already knew. Adoption was instant. The platform we wanted to use would have meant retraining the CA, and that conversation alone would have cost more than the platform did."

Frequently asked questions about online bill payment for businesses in India

1. What is BBPS and how does it work for businesses?

BBPS (Bharat Bill Payment System), now branded Bharat Connect, is India's centralised, RBI-regulated bill payment platform operated by NPCI Bharat BillPay. Businesses can pay utility, telecom, insurance, EMI, municipal and subscription bills from a single rail rather than logging into individual provider portals. RazorpayX, Cashfree and Paytm for Business offer BBPS through their dashboards; specialist tools like Tally Prime add it through a connector; bundled platforms include it natively. Settlements typically clear within 2–4 hours, and every transaction generates a receipt that can be reconciled to your accounting software.

2. Which bills can be paid through BBPS in India?

BBPS covers 22,000+ billers across electricity (DISCOMs), water, piped gas, LPG, telecom (postpaid and prepaid), broadband, DTH, insurance premiums, loan EMIs, credit card bills, FASTag, municipal taxes, housing society maintenance and a growing list of subscriptions. If your vendor is a registered service provider, the odds are very strong they are on the Bharat Connect network. Anything outside the BBPS scope typically B2B vendor invoices needs a separate workflow through NEFT, RTGS or a vendor payments tool such as RazorpayX or Cashfree.

3. Is BBPS secure for online bill payments?

Yes. BBPS is regulated by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007, and follows RBI's Master Directions on Payment Aggregators. All transactions are encrypted, two-factor authentication is mandatory for payouts above ₹15,000 from 1 April 2026, and audit logs are retained by the operating Payment Aggregator. For larger SMEs, add role-based access controls and IP whitelisting at the platform layer.

4. Can startups use BBPS for automating vendor payments?

BBPS is designed for payments to registered billers — utilities, telecom, insurers, municipal bodies, lenders. For B2B vendor invoices to small suppliers or freelancers, BBPS is not the right rail. RazorpayX Vendor Payments handles that workflow with TDS calculations and contractor-friendly approvals. A bundled platform handles both - BBPS for billers, direct transfers for vendors under the same approvals chain.

5. How do I integrate BBPS bill payment with my business accounting software?

The cleanest path is to use a platform that already integrates with your accounting tool. Zoho Books has native bill-payment workflows. Tally Prime needs a BBPS connector. QuickBooks and ERPs typically integrate through RazorpayX, Cashfree or bundled platform APIs. If you are building custom software, both Cashfree and PayU expose well-documented Bill Payment APIs you can wire into your own system.

6. What does a BBPS bill payment platform actually cost an SME?

BBPS itself charges ₹0–5 per transaction depending on the biller category. Platform fees layer on top: Bharat Connect direct is effectively free, Zoho Books from ₹749/month, Peko's SME tier from ₹999/month, RazorpayX and Cashfree charge per-transaction at roughly 1.75–2.5%. Most SMEs running 30+ monthly bills break even within two months on time saved alone, before counting reduced late fees.

7. Can we schedule recurring bill payments through BBPS?

Not through BBPS directly. The Bharat Connect rail processes individual payments. To schedule recurring debits you need a platform layer: Cashfree's UPI AutoPay handles e-NACH mandates up to ₹15,000 without OTP, RazorpayX supports scheduled vendor payouts, and bundled platforms typically support recurring schedules for any BBPS-eligible biller. SalaryBox handles deskless workforce payouts on a similar pattern. Set the schedule, set the approver, and let the system do the rest.

8. How long does a BBPS payment take to settle?

Most BBPS transactions clear to the biller within 2–4 hours. Some categories DISCOMs in particular may take up to 24 hours to reflect in the customer's account at the biller's end, even after the payment has cleared on the rail. Real-time status is visible on the payment platform; receipts carry a Bharat Connect reference number that the biller's helpdesk can trace.

9. Do bank corporate portals (ICICI, HDFC, Axis) support BBPS for SMEs?

Yes. Most major Indian bank corporate net-banking portals have BBPS modules built in. The benefit is that everything lives inside your existing banking relationship. The trade-off is user experience and reconciliation bank portals are functional rather than pleasant, and exporting an audit pack for a CA review takes more work than a purpose-built platform would. For finance teams with under 20 monthly bills, the bank portal is often the path of least resistance.

10. How do I claim GST input credit on BBPS bill payments?

Capture the biller's GSTIN at the time of payment, ensure the bill is issued in your business's GSTIN, and keep the BBPS receipt with the tax invoice. Utility, telecom and internet bills are typically eligible for input credit under the CGST Act, 2017. Refer to the latest input credit rules on the CBIC portal before relying on credit for any unusual category, especially fleet and insurance.

11. Does BBPS handle TDS on vendor payments?

BBPS does not handle TDS on the rail itself, because most BBPS payments are to billers (utilities, telecom, insurers) where TDS does not apply. For applicable categories under section 194 of the Income Tax Act - particularly rent, professional fees and contractor payments, the platform layer is what calculates TDS, generates the challan and adjusts the net payout. RazorpayX and bundled platforms handle this automatically; Zoho Books surfaces it inside the Bills module.

12. What is the difference between BBPS and UPI for business bill payments?

UPI is the underlying real-time payments rail, run by NPCI. BBPS is a bill-payment overlay that uses UPI (and net banking, cards, cash at agents) as the funding mechanism. For an SME, the practical difference is structure: UPI is a payment channel, BBPS is a structured bill-payment system with biller catalogues, fixed bill amounts, receipts and dispute resolution. You can pay a bill over UPI to a verified merchant; you can pay the same bill through BBPS and get a regulated receipt back.

13. How is BBPS regulated and audited?

BBPS is operated by NPCI Bharat BillPay under the Reserve Bank of India's Payment and Settlement Systems Act, 2007. The RBI publishes Master Directions on Payment Aggregators (most recently updated for 2026) and runs periodic system audits. Customer Operating Units (COUs) that route BBPS transactions must hold an RBI Payment Aggregator licence, verifiable on rbi.org.in.

14. Can a CA firm use BBPS for client bill payments at scale?

Yes, and many already do. Tally Prime with a BBPS connector is the workflow most CAs default to, because Tally remains the dominant accounting product in Indian CA practice. GreytHR is sometimes used for the payroll side. For larger CA firms managing 50+ client books, a bundled platform with multi-entity support is worth evaluating because it lets the firm see all client bill payments in one place without breaching client confidentiality.

15. Does BBPS support deskless workforces and field-service teams?

Indirectly. BBPS itself is a bill-payment system, not a field tool. SalaryBox, Asanify and other deskless-workforce tools handle the field-team layer (attendance, payouts, expense capture) and integrate with BBPS-aware platforms for the bill-payment side. If your business is field-heavy, logistics, services, retail with many small outlets - the question is less "which BBPS tool" and more "which workforce tool, with what BBPS integration".

16. What happens to BBPS if RBI changes the payment rules again?

Regulatory change is the second-biggest operational risk in Indian payments. The 1 April 2026 two-factor authentication mandate is the most recent example, and the 30 June 2026 Customer Operating Unit routing deadline is the next. Platforms with licensed PA status absorb most of the operational burden of these changes on behalf of their customers. If you choose an unlicensed reseller or a thin wrapper, you carry more of the risk yourself. Verify PA licence status before signing any contract.

17. Are there free BBPS bill payment platforms for very small businesses?

The official Bharat Connect web portal is effectively free —> ₹0–5 per transaction with no subscription. For businesses paying fewer than 15 bills a month, it remains the most economical option. The trade-off is the workflow: manual reconciliation, basic audit trail, no approvals, no native mobile app. The day your team grows past one finance owner, you will outgrow the free option.

Further reading from the Peko India hub

- Bill Payments for India - the BBPS-powered module described in this guide.

- Payroll & HR for India - PF, ESI, TDS and Form 24Q handling.

- Corporate Travel for India - travel bookings and reimbursements in the same finance dashboard.

- Compliance for India - statutory deadline tracking and filing support.

- India pricing - transparent SME tiers from ₹999/month.

- India home - the all-in-one SME platform for SMEs.

- Partner with Peko - for CAs, consultants and resellers.

- GST compliance calendar for Indian SMEs 2026 - paired calendar resource.

- Bill Payment Compliance Calendar 2026 PDF - free download.

A final note on trust and methodology

This guide is written by the team that builds Peko. We are not neutral, and we have made our scoring criteria, weighting and trade-offs explicit so you can re-rank the list for your own situation. Every competitor here is genuinely good at something; every one of them, including us, has at least one axis where another platform does better. The point of an honest buyer's guide is not to crown a winner — it is to help you ask the right questions when a sales team calls. If you have read this far and we have earned a 30-minute conversation, our team in India is happy to walk through your bill mix in detail. If we are not the right fit, we will say so and recommend who is.

Sources: RBI Master Directions on Payment Aggregators (rbi.org.in); NPCI BBPS / Bharat Connect statistics (bharat-connect.com); Income Tax Act, 1961, s. 194 (incometax.gov.in); CGST Act, 2017 (cbic-gst.gov.in); EPFO (epfindia.gov.in); ESIC (esic.gov.in); Ministry of Labour & Employment (labour.gov.in); Press Information Bureau (pib.gov.in). Peko internal benchmarks: 84 customer cycles, January–December 2025. All figures reviewed by the Bill Payments Team in May 2026.